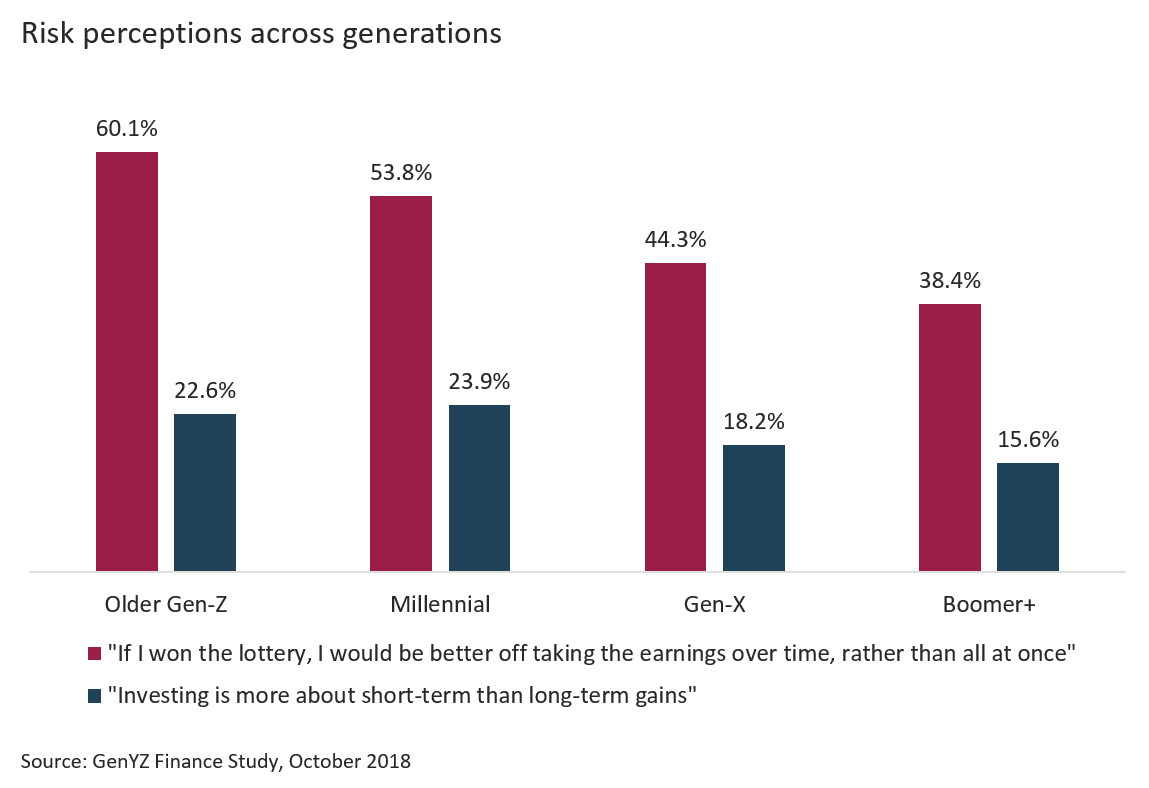

Risk aversion is getting younger.

Traditionally, our society has always considered the younger generations to be less aware of financial risk. We associate younger life stages with being carefree, but our newest study suggests that Gen Z is coming into adulthood with a surprisingly strong awareness of debt and financial risk.

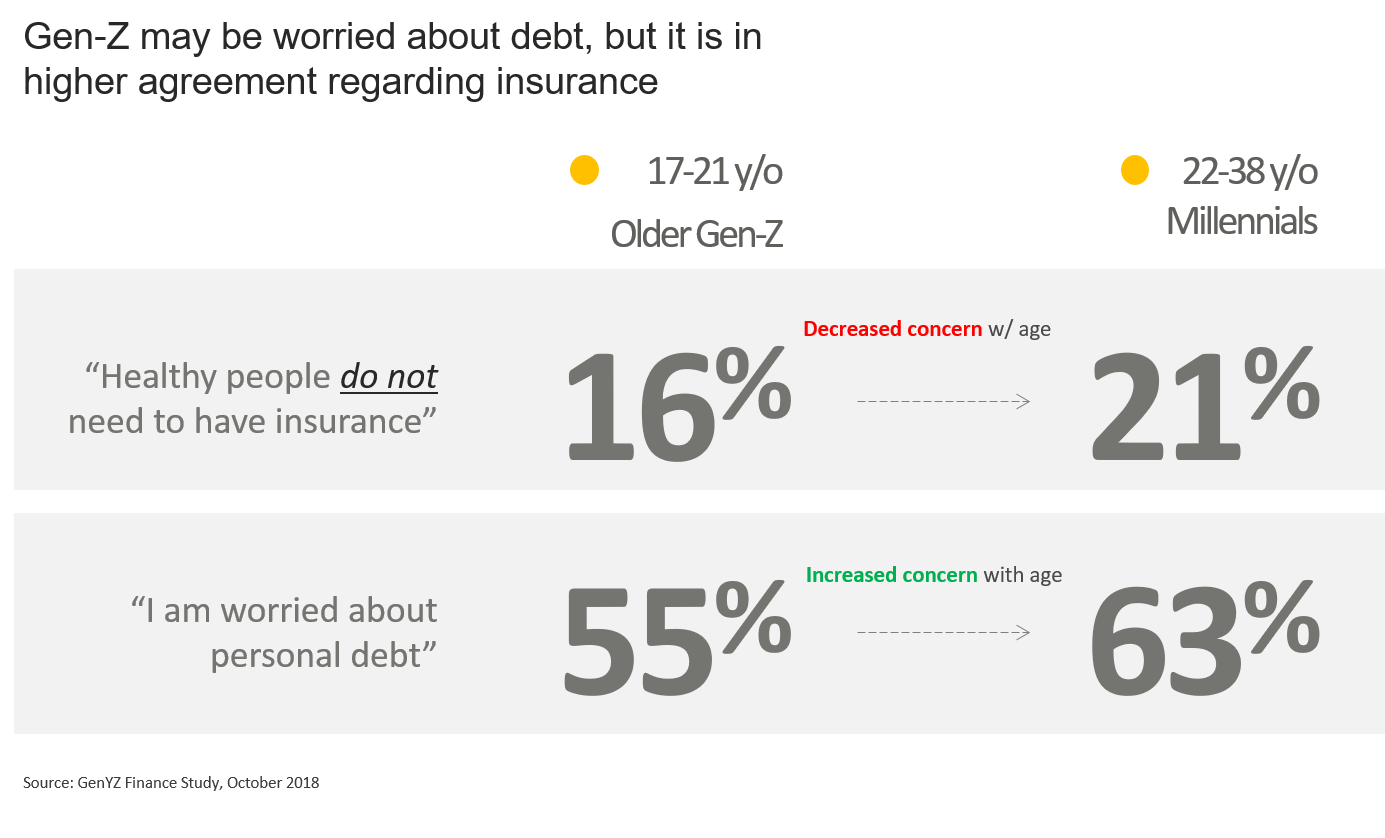

Over half of college-aged Gen Zs are already worried about personal debt. They are also remarkably likely to disagree with the idea that healthy people do not need insurance. These data points contradict what we have typically understood about the behavior of young consumers, suggesting that we should keep a closer eye on this generation’s emerging financial profile.

Our previous research suggests that financial anxiety may be more common than you think with younger consumers, and it’s important to understand the events that have shaped this wariness.

Born and raised in the wake of the recession, Gen Z individuals have lived through an economic downfall that pervasively reduced trust in large financial institutions. And with the cost of education on the rise, Gen Z is also faced with impending student loans. If they have Millennial siblings, they may have been directly exposed to debt burdens unlike those experienced by any prior generation. This could explain why they’re more likely to take responsible positions regarding future oriented finance decisions.

Gen Z’s hypersensitive financial profile fuels their demand for innovative solutions.

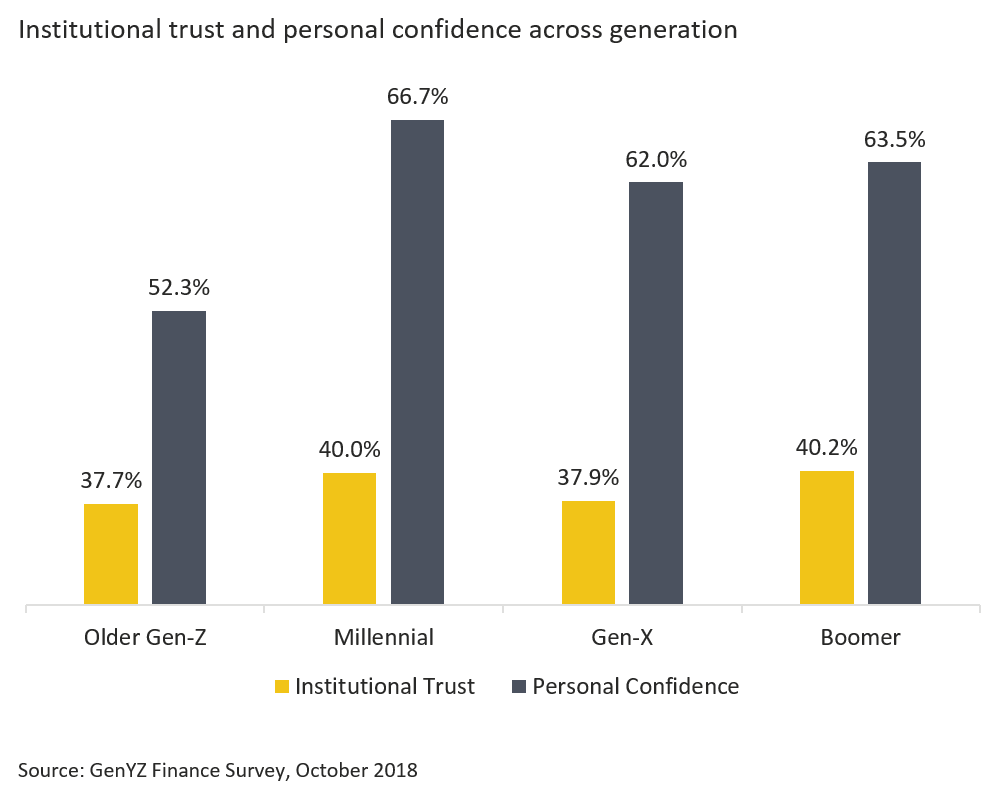

Gen Z risk aversion is compounded by their lack of confidence in making financial decisions. Conventionally, this combination would make them an ideal target for established financial institutions. But Gen Z just don’t see big institutions as the partners that will be helpful for building that confidence and reaching their goals.

That poses the question: how do you market financial services to people who don’t trust large institutions – and by the way have only a minimal relationship with a traditional provider? Look to Fintech for lessons. FinTech start-ups have successfully tapped into Gen Z’s risk-averse mentality and tech-savvy nature by offering a variety of apps and platforms that ease the process of investing and saving money.

Now that Gen Z is on the cusp of assuming major financial responsibilities, incumbent financial service providers are under pressure to cater to their financial anxieties – but face stiff competition. Here’s how some of these new entrants are offering Gen Zs an attractive solution:

Acorns

By making automated micro-investments, Acorns solves the generational confidence problem with managing money: it integrates investing into daily spending behavior without any added decision-making.

Zelle

With only three steps required to complete a transaction, Zelle takes the guesswork out of splitting checks and transferring money. Gen Z is a tech savvy generation, which means Zelle fits in with their lifestyle seamlessly.

Robinhood

Robinhood levels the playing field for cost conscious Gen Z with zero-fee investments. It replaces the role of big financial institutions and makes the stock market a friendlier turf for anyone who wants to invest in the stock market.

Wealthfront

For super-sensitive financial profiles like Gen Z, Wealthfront delivers a simple and structured financial plan. The interface provides clear-cut recommendations on purchase decisions and budgeting.

4550 Montgomery Avenue Bethesda, Maryland, 20814

(240) 482-8260